No. 26/201/DKom

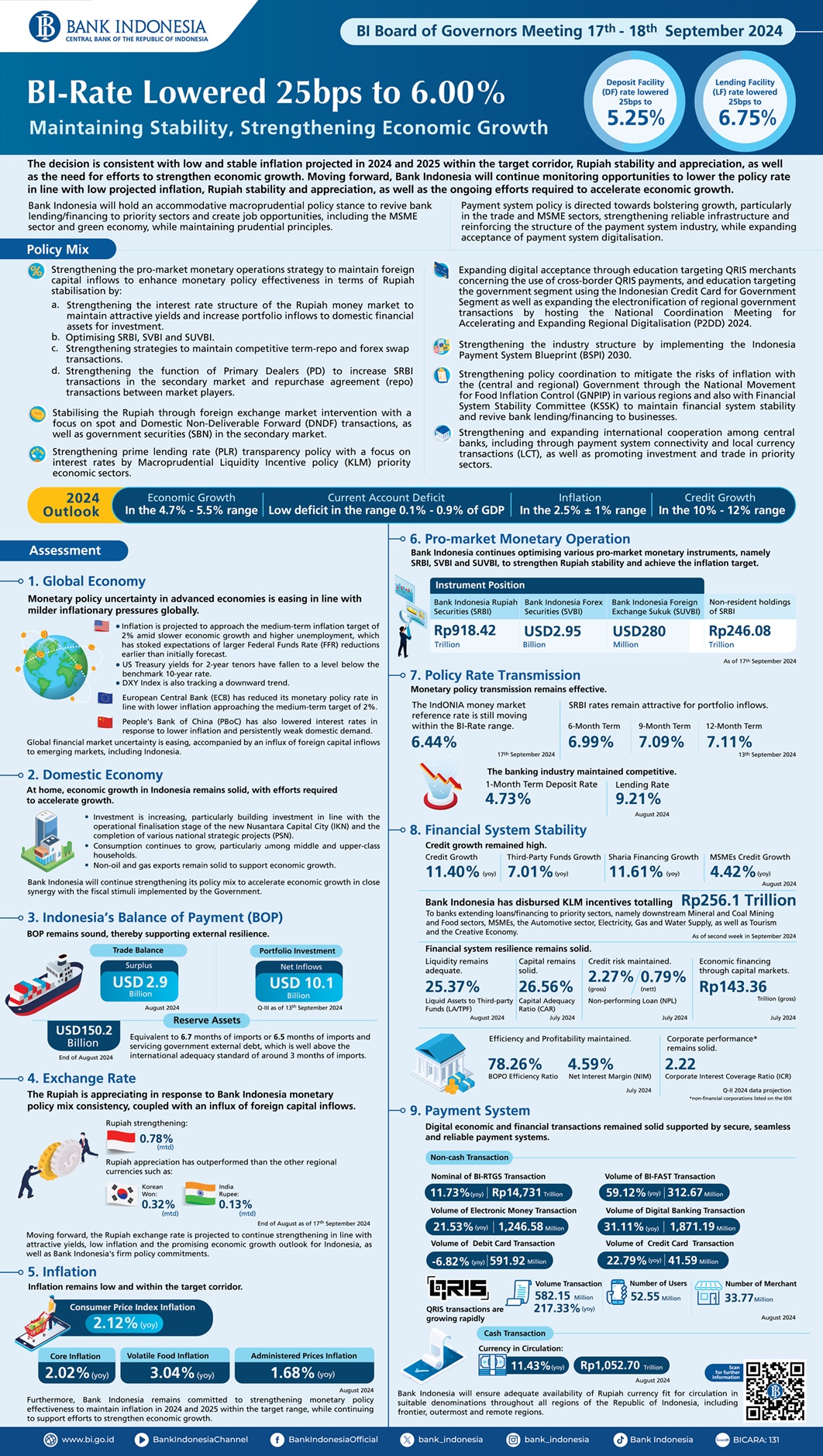

The BI Board of Governors Meeting agreed on 17-18th September 2024 to lower the BI-Rate by 25bps to 6.00%, while also lowering the Deposit Facility (DF) rate and Lending Facility (LF) rate by 25bps to 5.25% and 6.75% respectively. The decision is consistent with low and stable inflation projected in 2024 and 2025 within the 2.5±1% target corridor, Rupiah stability and appreciation, as well as the need for efforts to strengthen economic growth. Moving forward, Bank Indonesia will continue monitoring opportunities to lower the policy rate in line with low projected inflation, Rupiah stability and appreciation, as well as the ongoing efforts required to accelerate economic growth. Meanwhile, Bank Indonesia will maintain pro-growth macroprudential and payment system policies to foster sustainable economic growth. Bank Indonesia will hold an accommodative macroprudential policy stance to revive bank lending/financing to priority sectors and create job opportunities, including the MSME sector and green economy, while maintaining prudential principles. Payment system policy is directed towards bolstering growth, particularly in the trade and MSME sectors, strengthening reliable infrastructure and reinforcing the structure of the payment system industry, while expanding acceptance of payment system digitalisation.

Bank Indonesia has, therefore, strengthened its monetary, macroprudential and payment system policy mix to maintain stability and support sustainable economic growth through the following measures:

- Strengthening the pro-market monetary operations strategy to maintain foreign capital inflows to enhance monetary policy effectiveness in terms of Rupiah stabilisation by:

- Strengthening the interest rate structure of the Rupiah money market to maintain attractive yields and increase portfolio inflows to domestic financial assets for investment.

- Optimising Bank Indonesia Rupiah Securities (SRBI), Bank Indonesia Foreign Exchange Securities (SVBI) and Bank Indonesia Foreign Exchange Sukuk (SUVBI).

- Strengthening strategies to maintain competitive term-repo and forex swap transactions, and

- Strengthening the function of Primary Dealers (PD) to increase SRBI transactions in the secondary market and repurchase agreement (repo) transactions between market players.

- Stabilising the Rupiah through foreign exchange market intervention with a focus on spot and Domestic Non-Deliverable Forward (DNDF) transactions, as well as government securities (SBN) in the secondary market.

- Strengthening prime lending rate (PLR) transparency policy with a focus on interest rates by Macroprudential Liquidity Incentive policy (KLM) priority economic sectors (Appendix).

- Expanding digital acceptance through education targeting QRIS merchants concerning the use of cross-border QRIS payments, and education targeting the government segment using the Indonesian Credit Card for Government Segment as well as expanding the electronification of regional government transactions by hosting the National Coordination Meeting for Accelerating and Expanding Regional Digitalisation (P2DD) 2024; and

- Strengthening the industry structure by implementing the Indonesia Payment System Blueprint (BSPI) 2030 through increased competency certification in the payment system industry.

Policy coordination between Bank Indonesia and the Government is also constantly strengthened to maintain stability and strengthen economic growth. Policy coordination with the (central and regional) Government is strengthened through the National Movement for Food Inflation Control (GNPIP) in various regions within the Central Government and Regional Government Inflation Control Teams (TPIP and TPID). Monetary and fiscal policy coordination is also strengthened to maintain macroeconomic stability and bolster economic growth momentum. Furthermore, policy synergy between Bank Indonesia and the Financial System Stability Committee (KSSK) is also strengthened to maintain financial system stability and revive bank lending/financing to businesses. Bank Indonesia is strengthening and expanding international cooperation among central banks, including through payment system connectivity and local currency transactions (LCT), as well as promoting investment and trade in priority sectors in synergy with relevant institutions.

Monetary policy uncertainty in advanced economies is easing in line with milder inflationary pressures globally. In the United States (US), inflation is projected to approach the medium-term inflation target of 2% amid slower economic growth and higher unemployment. The current state of the US economy has stoked expectations of larger Federal Funds Rate (FFR) reductions earlier than initially forecast. Furthermore, US Treasury yields for 2-year tenors have fallen to a level below the benchmark 10-year rate, while the DXY Index is also tracking a downward trend. In Europe, the European Central Bank (ECB) has reduced its monetary policy rate in line with lower inflation approaching the medium-term target of 2%. In Asia, the People's Bank of China (PBoC) has also lowered interest rates in response to lower inflation and persistently weak domestic demand. Consequently, global financial market uncertainty is easing, accompanied by an influx of foreign capital inflows to emerging markets, including Indonesia. Moving forward, further clarification regarding interest rate reductions in advanced economies, the US in particular, will boost foreign capital inflows and strengthen external stability in emerging market and developing economies (EMDEs). This will support economic policy in EMDEs for domestic economic goals in terms of maintaining stability and fostering economic growth.

At home, economic growth in Indonesia remains solid, with efforts required to accelerate growth. Investment is increasing, particularly building investment in line with the operational finalisation stage of the new Nusantara Capital City (IKN) and the completion of various national strategic projects (PSN). Consumption continues to grow, particularly among middle and upper-class households. Non-oil and gas exports remain solid to support economic growth. Government expenditures, which are forecast to increase towards yearend, are also expected to bolster domestic demand. Based on the latest indicators, including the results of Bank Indonesia surveys, economic activity in the third quarter of 2024 remains solid, as reflected by high consumer confidence, positive retail sales performance, as well as increasing capital goods imports and cement sales. Bank Indonesia projects economic growth in 2024 in the 4.7-5.5% range. Moving forward, various efforts must be maintained to nurture growth from the demand and supply sides. To that end, Bank Indonesia will continue strengthening its policy mix to accelerate economic growth in close synergy with the fiscal stimuli implemented by the Government. On the supply side, structural reforms must be strengthened to increase productivity and strengthen the economic growth structure, including economic sectors with high labour absorption and value added.

Indonesia's Balance of Payments (BOP) remains sound, thereby supporting external resilience. The BOP deficit narrowed in the second quarter of 2024 given the capital and financial account surplus and manageable current account deficit. BOP performance has continued to improve in the third quarter of 2024, supported by a maintained positive trade balance which amassed a USD2.9 billion surplus in August 2024. Meanwhile, portfolio inflows remain high, recording a net inflow of USD10.1 billion (qtd) in the third quarter of 2024 (as of 13th September 2024) across all domestic financial instruments. Furthermore, the position of foreign reserves at the end of August 2024 increased to USD150.2 billion, equivalent to 6.7 months of imports or 6.5 months of imports and servicing government external debt, which is well above the international adequacy standard of around 3 months of imports. Moving forward, BOP performance in 2024 is projected to be maintained, underscored by a low and manageable current account deficit in the 0.1%-0.9% of GDP range. On the other hand, the capital and financial account surplus is expected to widen given maintained foreign capital inflows as global financial market uncertainty continues to improve, positive investor perception concerning the promising domestic economic outlook and attractive yields on financial assets for investment.

The Rupiah is appreciating in response to Bank Indonesia monetary policy mix consistency, coupled with an influx of foreign capital inflows. The Rupiah in September 2024 (as of 17th September 2024) appreciated to Rp15,330/USD, improving 0.78% on the position recorded at the end of August 2024. Rupiah appreciation has outperformed other regional currencies, including the South Korean won and Indian rupee that appreciated by 0.32% and 0.13%, respectively. Compared with the level recorded at the end of December 2023, therefore, the Rupiah has appreciated 0.40% in contrast to the depreciation experienced by the Indian rupee and South Korean won at 0.66% and 3.41%. Moving forward, the Rupiah exchange rate is projected to continue strengthening in line with attractive yields, low inflation and the promising economic growth outlook for Indonesia, as well as Bank Indonesia's firm policy commitments. Furthermore, Bank Indonesia continues optimising the full panoply of monetary instruments available, which includes strengthening its pro-market monetary operations strategy through the SRBI, SVBI and SUVBI instruments to boost policy effectiveness in terms of attracting foreign capital inflows and supporting efforts to strengthen the Rupiah exchange rate.

Inflation remains low and within the 2.5±1% target corridor. Low Consumer Price Index (CPI) inflation was recorded in August 2024 at 2.12% (yoy), influenced by all components. Core inflation was recorded at 2.02% (yoy), while volatile food inflation continued falling to 3.04% (yoy) from 3.63% (yoy) the month earlier. Lower volatile food inflation was recorded in most Indonesian regions in response to increasing food supply during the ongoing harvesting season, coupled with the positive impact of close synergy to manage inflation between the TPIP/TPID teams through the GNPIP movement. Moving forward, Bank Indonesia is confident that CPI inflation will remain under control and within the target corridor. Core inflation is projected to remain under control in line with anchored inflation expectations, massive economic capacity in response to domestic demand, low imported inflation in line with Rupiah stability by Bank Indonesia, as well as the positive impact of digitalisation. Bank Indonesia also expects volatile food inflation to remain manageable, underpinned by inflation control synergy between Bank Indonesia and the (central and regional) Government. Furthermore, Bank Indonesia remains committed to strengthening monetary policy effectiveness to maintain inflation in 2024 and 2025 within the 2.5±1% target range, while continuing to support efforts to strengthen economic growth.

Bank Indonesia continues optimising various pro-market monetary instruments, namely SRBI, SVBI and SUVBI, to strengthen Rupiah stability and achieve the inflation target. This policy also aims to accelerate money market deepening efforts and attract foreign capital inflows. As of 17th September 2024, the respective positions of SRBI, SVBI and SUVBI instruments stood at Rp918.42 trillion, USD2.95 billion and USD280 million. SRBI issuances have attracted portfolio inflows to Indonesia and strengthened the Rupiah, as reflected by significant non-resident holdings of SRBI totalling Rp246.08 trillion (26.79% of total outstanding). The implementation of Primary Dealers (PD) since May 2024 has also increased SRBI transactions in the secondary market along with repurchase agreement (repo) transactions between market players, thereby strengthening the effectiveness of monetary instruments that support Rupiah stability and inflation control. Moving forward, Bank Indonesia will continue optimising its various innovative pro-market instruments in terms of volume and attractive yields, strengthened by solid economic fundamentals, in pursuit of further portfolio inflows to domestic financial markets.

Monetary policy transmission remains effective. The IndONIA money market reference rate is still moving within the BI-Rate range, recorded at 6.44% on 17th September 2024. SRBI rates remain attractive at 6.99%, 7.09% and 7.11% for tenors of 6, 9 and 12 months, respectively, as of 13th September 2024. SBN yields on tenors of 2 and 10 years decreased to 6.47% and 6.55%, respectively, as of 17th September 2024, triggered by increasing demand from non-residents in line with a surge of foreign capital inflows to the SBN market. Meanwhile, liquidity in the banking industry remains ample in line with implementation of the Bank Indonesia policy mix, including Macroprudential Liquidity Incentives (KLM). Adequate liquidity and pricing efficiency in the banking industry are consistent with PLR transparency policy, which has had a positive impact on competitive interest rates in the banking industry. The 1-month term deposit rate and lending rate were also relatively stable in August 2024 at 4.73% and 9.21%, respectively.

Credit growth remained high in August 2024, reaching 11.40% (yoy). On the supply side, bank lending appetite was maintained in line with adequate funding, the ongoing bank strategy to reallocate liquid assets to credit, and policy support from Bank Indonesia in the form of Macroprudential Liquidity Incentive policy (KLM). As of the second week of September 2024, Bank Indonesia has disbursed KLM incentives totalling Rp256.1 trillion, including to state-owned banks (Rp118.6 trillion), national private commercial banks (Rp110.5 trillion), regional government banks (Rp24.4 trillion) and foreign bank branches (Rp2.6 trillion). The KLM incentives are disbursed to banks extending loans/financing to priority sectors, namely downstream Mineral and Coal Mining and Food sectors, MSMEs, the Automotive sector, Electricity, Gas and Water Supply, as well as Tourism and the Creative Economy. On the demand side, loan growth is supported by robust corporate demand, particularly in capital-intensive industries, while corporate demand for loans in labour-intensive sectors must be improved further. Meanwhile, household demand for loans remains strong, particularly for housing loans. Credit growth remains high in most economic sectors, particularly the Manufacturing Industry, Electricity, Gas and Water as well as Transportation. By loan type, credit growth is primarily supported by working capital loans, investment loans and consumer loans, growing 10.75% (yoy), 13.08% (yoy) and 10.83% (yoy), respectively, in August 2024. Furthermore, sharia financing recorded 11.61% (yoy) growth, while MSME loans increased 4.42% (yoy) in the reporting period. Consequently, Bank Indonesia projects credit growth to increase towards the upper bound of the 10-12% range in 2024. Bank Indonesia will also continue strengthening KLM implementation, embracing sectors that support job creation, new sources of economic growth (tertiary sectors) and sectors that can increase inclusivity, including the lower-middle class, while maintaining prudential principles.

Financial system resilience remains solid. Bank liquidity remained adequate in August 2024, as reflected by a high ratio of liquid assets to third-party funds (LA/TPF) at 25.37%. The Capital Adequacy Ratio (CAR) also remained high in July 2024 at 26.56%, thereby absorbing risk and supporting credit growth effectively. Meanwhile, non-performing loans (NPL), as a proxy of credit risk, were also low in July 2024, as indicated by NPL ratios of 2.27% (gross) and 0.79% (nett). Banking industry resilience in terms of capital and liquidity was also supported by maintained repayment capacity and corporate profitability, as confirmed by the latest BI stress tests. Moving forward, Bank Indonesia will continue strengthening synergy with KSSK to mitigate various risks that could potentially disrupt financial system stability.

Digital economic and financial transactions remained solid in August 2024, supported by secure, seamless and reliable payment systems. On the wholesale or high-value side, BI-RTGS transactions increased 11.73% (yoy) to reach Rp14,731 trillion. On the other hand, the volume of retail transactions processed through BI-FAST increased 59.12% (yoy) to 312.67 million transactions. The volume of digital banking transactions was recorded at 1,871.19 million, growing 31.11% (yoy), while the volume of electronic money transactions grew 21.53% (yoy) to reach 1,246.58 million. The volume of card-based payments using ATM/debit cards retreated 6.82% (yoy) to 591.92 million transactions and credit card transactions increased 22.79% (yoy) to reach 41.59 million. QRIS transactions enjoyed impressive 217.33% (yoy) growth, with QRIS users and merchants totalling 52.55 million and 33.77 million, respectively. In terms of Rupiah currency management, total currency in circulation grew 11.43% (yoy) to Rp1,052.70 trillion.

Payment system stability has been maintained, supported by a stronger structure and resilient infrastructure. In terms of infrastructure, Bank Indonesia maintains a seamless and reliable payment system (SPBI). Regarding the structure of the payments industry, payment system interconnection and the digital economy and finance ecosystem continue to expand. Payment transactions based on the National Open API Payment Standard (SNAP), which facilitates interconnection in the payment system, continue to grow as SNAP adoption among various industry players expands. As one of the initiatives of BSPI 2030, on 11th September 2024, Bank Indonesia recognised the Certification Institute for Payment System Professionals (LSP SPI) as the professional certification institute authorised for the payment system in Indonesia. LSP SPI was established by the Indonesia Payment System Association (ASPI), which represents the payment system industry, and is expected to play an active role in creating competent payment system professionals with the requisite knowledge, skills and attitude to face the emerging payment system challenges in the digital era. Meanwhile, Bank Indonesia will ensure adequate availability of Rupiah currency fit for circulation in suitable denominations throughout all regions of the Republic of Indonesia, including frontier, outermost and remote regions.

Jakarta, 18th September 2024

Communication Department

Erwin Haryono

Governor Assistant