No. 23/ 177 /DKom

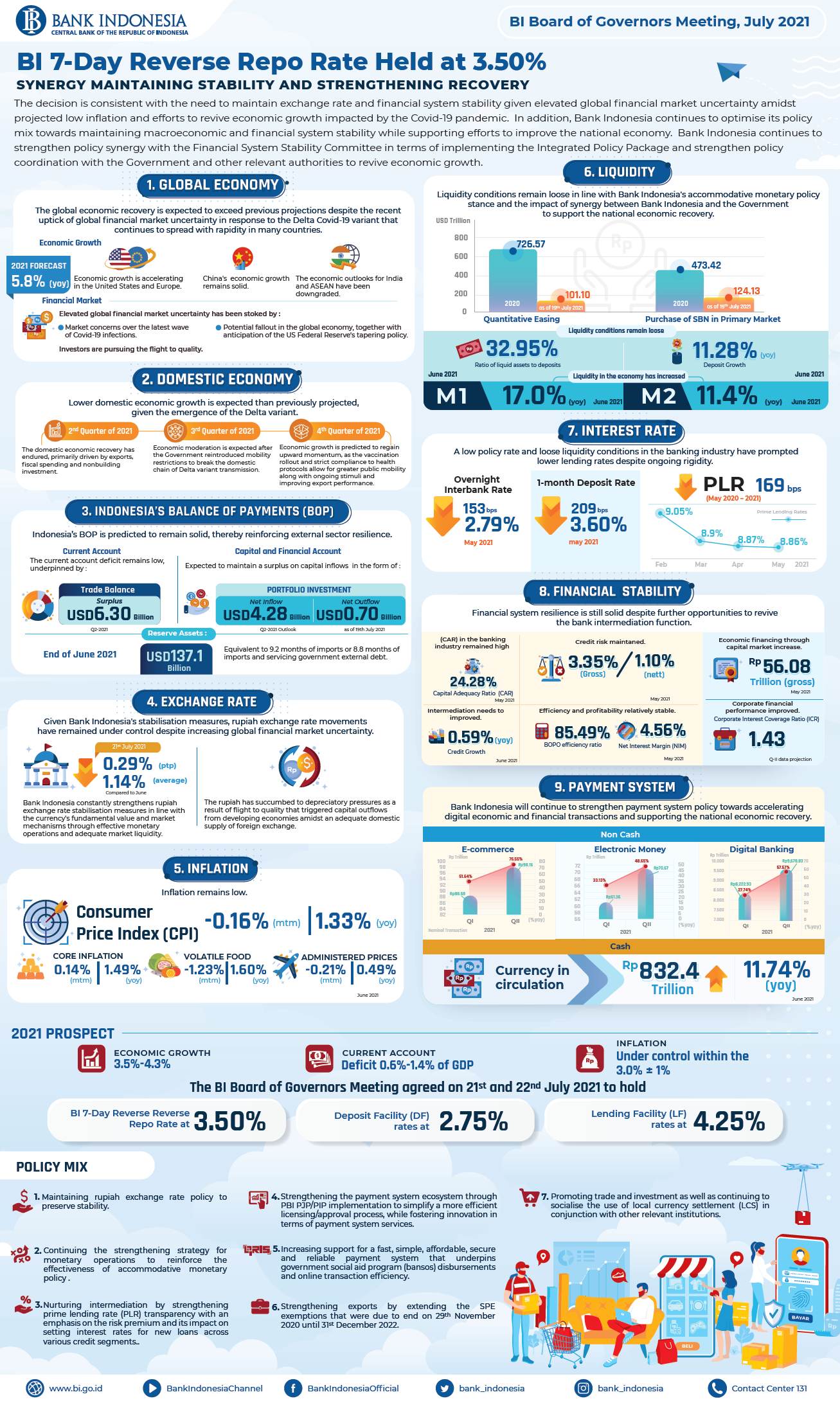

The BI Board of Governors Meeting agreed on 21st and 22nd July 2021 to hold the BI 7-Day Reverse Repo Rate at 3.50%, while also maintaining the Deposit Facility (DF) rates at 2.75% and Lending Facility (LF) rates at 4.25% The decision is consistent with the need to maintain exchange rate and financial system stability given elevated global financial market uncertainty amidst projected low inflation and efforts to revive economic growth impacted by the Covid-19 pandemic. In addition, Bank Indonesia continues to optimise its policy mix towards maintaining macroeconomic and financial system stability, while supporting efforts to improve the national economy through the following measures:

- Maintaining rupiah exchange rate policy to preserve stability in line with the currency's fundamental value and market mechanisms.

- Continuing the strengthening strategy for monetary operations to reinforce the effectiveness of accommodative monetary policy.

- Nurturing intermediation by strengthening prime lending rate (PLR) transparency with an emphasis on the risk premium and its impact on setting interest rates for new loans across various credit segments (appendix).

- Strengthening the payment system ecosystem through PBI PJP/PIP implementation to simplify a more efficient licensing/approval process, while fostering innovation in terms of payment system services.

- Increasing support for a fast, simple, affordable, secure and reliable payment system that underpins government social aid program (bansos) disbursements and online transaction efficiency.

- Strengthening exports by extending the SPE exemptions that were due to end on 29th November 2020 until 31st December 2022 in order to exploit increasing demand in trading partner countries as well as rising international commodity prices.

- Promoting trade and investment as well as continuing to socialise the use of local currency settlement (LCS) in conjunction with other relevant institutions. In July and August 2021, Bank Indonesia will promote trade and investment in Japan, United States, Sweden and Singapore.

Bank Indonesia continues to strengthen policy synergy with the Financial System Stability Committee in terms of implementing the Integrated Policy Package to maintain financial system stability and stimulate lending to the corporate sector and other priority sectors, including micro, small and medium enterprises (MSME). Bank Indonesia will also strengthen policy coordination with the Government and other relevant authorities to revive economic growth, including monetary-fiscal policy coordination, export stimuli as well as economic and financial inclusion.

The global economic recovery is expected to exceed previous projections despite the recent uptick of global financial market uncertainty in response to the Delta Covid-19 variant that continues to spread with rapidity in many countries. Economic growth is accelerating in the United States and Europe given the rapid vaccination rollout, coupled with fiscal and monetary stimuli, while growth in China remains solid. The economic outlooks for India and ASEAN have been downgraded, however, in line with the reintroduction of mobility restrictions to overcome a new wave of Covid-19 cases. In line with the recovery, Bank Indonesia has upgraded its global economic growth outlook for 2021 to 5.8% from 5.7%. World trade volume and international commodity prices are also expected to rise, thus supporting stronger export performance in developing economies, including Indonesia. Nevertheless, elevated global financial market uncertainty has been stoked by market concerns over the latest wave of Covid-19 infections and potential fallout in the global economy, together with anticipation of the US Federal Reserve's tapering policy. In response, investors are pursuing the flight to quality, hence restraining capital flows and intensifying currency pressures in developing economies, including Indonesia.

At home, lower domestic economic growth is expected than previously projected, given the emergence of the Delta variant. As of the second quarter of 2021, the domestic economic recovery has endured, primarily driven by exports, fiscal spending and nonbuilding investment. Early indicators in June 2021, including retail sales and PMI, confirmed an ongoing economic recovery. Notwithstanding, economic moderation is expected in the third quarter of 2021 after the Government reintroduced mobility restrictions to break the domestic chain of Delta variant transmission. Household consumption has been severely undermined by emergency mobility restrictions despite increasing social aid program (bansos) disbursements from the Government and persistently solid export performance. Economic growth is predicted to regain upward momentum in the fourth quarter of 2021 as the vaccination rollout and strict compliance to health protocols allow for greater public mobility along with ongoing stimuli and improving export performance. Regionally, less economic moderation has been recorded outside Java, particularly in Sulawesi-Maluku-Papua (Sulampua), supported by strong export performance. Consequently, Bank Indonesia has revised down its national economic growth projection for 2021 to 3.5-4.3% from 4.1-5.1% previously.

Indonesia's Balance of Payments (BOP) is predicted to remain solid, thereby reinforcing external sector resilience. The current account deficit remains low and manageable, underpinned by an increase in the trade surplus to USD6.30 billion from USD5.56 billion in the previous period. Higher exports of major commodities, such as crude palm oil (CPO), coal, iron and steel as well as motor vehicles, coupled with rising international commodity prices have contributed to the larger trade surplus. The Sumatra, Sulampua and Java regions have recorded strong export performance. Meanwhile, the capital and financial account is also expected to maintain a surplus on capital inflows in the form of foreign capital investment and portfolio investment. In the second quarter of 2021, portfolio investment recorded a net inflow totalling USD4.28 billion. Entering the third quarter (as of 19th July 2021), however, portfolio investment recorded a net outflow of USD0.70 billion in response to elevated global financial market uncertainty. The position of reserve assets at the end of June 2021 stood at USD137.1 billion, equivalent to 9.2 months of imports or 8.8 months of imports and servicing government external debt, which is well above the 3-month international adequacy standard. Looking ahead, Bank Indonesia projects a low and manageable current account deficit in 2021 at approximately 0.6-1.4% of GDP, thus supporting external sector resilience in Indonesia.

Given Bank Indonesia's stabilisation measures, rupiah exchange rate movements have remained under control despite increasing global financial market uncertainty. As of 21st July 2021, the rupiah depreciated 1.14% on average and by 0.29% (ptp) on the June 2021 level. The rupiah has succumbed to depreciatory pressures as a result of flight to quality that triggered capital outflows from developing economies amidst an adequate domestic supply of foreign exchange. Consequently, as of 21st July 2021, the rupiah depreciated by approximately 3.39% (ytd) on the level recorded at the end of 2020, lower than depreciation in several other peer countries, including the Philippines, Malaysia and Thailand. Bank Indonesia constantly strengthens rupiah exchange rate stabilisation measures in line with the currency's fundamental value and market mechanisms through effective monetary operations and adequate market liquidity.

Inflation remains low. In June 2021, the Consumer Price Index (CPI), stood at 0.16% (mtm) deflation, bringing consumer price inflation for the year to 0.74% (ytd). Annually, CPI was recorded at 1.33% (yoy), down from 1.68% (yoy) one month earlier. Core inflation remains low and under control in line with subdued domestic demand, exchange rate stability and consistent Bank Indonesia policy to anchor inflation expectations to the target corridor. Milder inflationary pressures were recorded on volatile foods and administered prices as seasonal demand normalises after the recent national religious holidays (HBKN) amidst maintained supply. Bank Indonesia remains firmly committed to maintaining price stability and strengthening policy coordination with the central and regional governments through national and regional inflation control teams (TPI and TPID) to safeguard supply during mobility restrictions. Therefore, Bank Indonesia projects inflation within the 3.0%±1% target corridor in 2021 and 2022.

Liquidity conditions remain loose in line with Bank Indonesia's accommodative monetary policy stance and the impact of synergy between Bank Indonesia and the Government to support the national economic recovery. Bank Indonesia has injected liquidity through quantitative easing to the banking industry totalling Rp101.10 trillion in 2021 (as of 19th July 2021). In addition, Bank Indonesia continues to purchase SBN in the primary market as an integral part of policy synergy between Bank Indonesia and the Government to fund the 2021 State Revenue and Expenditure Budget (APBN). As of 19th July 2021, Bank Indonesia purchased SBN in the primary market totalling Rp124.13 trillion, consisting of Rp48.67 trillion through primary auction and Rp75.46 trillion through greenshoe options (GSO). Expansive monetary policy supports loose economic liquidity conditions, as reflected by the high ratio of liquid assets to deposits at 32.95% and deposit growth of 11.28% (yoy). Liquidity in the economy has also increased, as indicated by narrow (M1) and broad (M2) money supply, which grew 17.0% (yoy) and 11.4% (yoy) in June 2021. The main drivers of money supply growth are expansive policies by the authorities and credit growth, which has moved into positive territory. Moving ahead, increasing lending activity is expected to expand the contribution of liquidity in terms of driving economic growth through a higher velocity of money in the economy.

A low policy rate and loose liquidity conditions in the banking industry have prompted lower lending rates despite ongoing rigidity. In the markets, the overnight interbank rate and 1-month deposit rate have fallen by 153bps and 209bps respectively since May 2020 to 2.79% and 3.60% in May 2021. In the credit market, the banking industry continues to lower prime lending rates despite rigidity, thus falling 169bps since May 2020 to 8.86% in May 2021. A lower cost of loanable funds (CoLF) continues to drive down prime lending rates, while higher profit margins persist at foreign bank branches and state-owned banks. On the other hand, the risk premium has begun to trend downwards, indicating an improvement in the risk perception of the banking industry concerning the corporate sector. Furthermore, the lower risk premium has facilitated lower interest rates on new loans across all bank groups, except national private commercial banks. By loan type, the most significant decline of interest rates on new loans was recorded on microloans, followed by investment loans and working capital loans. Bank Indonesia expects the banking industry to continue lowering lending rates as part of the shared responsibility to stimulate lending to the corporate sector.

Financial system resilience is still solid despite further opportunities to revive the bank intermediation function. The Capital Adequacy Ratio (CAR) in the banking industry remained high in May 2021 at 24.28%, accompanied by persistently low NPL ratios of 3.35% (gross) and 1.10% (nett). Boosted by loose liquidity conditions and lower interest rates on new loans, the bank intermediation function charged into positive territory in June 2021 at 0.59% (yoy), although the opportunity for further growth remains. The recent gains stem from stronger demand for loans driven by the ongoing recovery in the corporate, household and MSME sectors. On the supply side, banking industry propensity to loosen lending standards, as reflected by a lower Lending Standards Index (LSI), contributed to positive credit growth. Nevertheless, the credit growth outlook for the third quarter of 2021 has been downgraded in line with less economic activity due to mobility restrictions before rebounding in the fourth quarter of 2021. Therefore, Bank Indonesia projects credit growth in 2021 at 4-6% and deposit growth at 6-8%. Furthermore, Bank Indonesia continues to strengthen policy synergy with the Financial System Stability Committee to implement the Integrated Policy Package, maintain financial system stability and stimulate loans/financing to the corporate sector and other priority sectors, including MSMEs.

Bank Indonesia will continue to strengthen payment system policy towards accelerating digital economic and financial transactions and supporting the national economic recovery. Growth of digital economic and financial transactions remains high given greater public acceptance and growing public preference towards online shopping as well as the expansion of digital payments and digital banking. The value of e-commerce transactions in the first and second quarters of 2021 increased 63.36% (yoy) to Rp186,75 trillion, with growth for 2021 projected to reach 48.4%, totalling Rp395 trillion. The value of electronic money transactions in the first and second quarters of 2021 increased 41.01% (yoy) to Rp132.03 trillion, with growth for 2021 projected to reach 35.7%, totalling Rp278trillion. Similarly, the value of digital banking transactions in the first and second quarters of 2021 increased 39.39% (yoy) to Rp17,901.76 trillion, with growth for 2021 projected to reach 30.1%, totalling Rp35,600 trillion. Bank Indonesia continues to accelerate payment system policy implementation in accordance with the Indonesia Payment System Blueprint 2025 in order to support development of an inclusive and efficient digital economy and finance by increasing QRIS transactions and expanding QRIS merchants, disbursing social aid program (bansos) benefits and strengthening the payment system ecosystem. On the cash side, currency in circulation in June 2021 stood at Rp832.4 trillion, up 11.74% (yoy) on the previous period. Bank Indonesia continues to safeguard the availability of rupiah banknotes and coins throughout the territory of the Republic of Indonesia based on public demand, while applying strict health protocols.

Jakarta, 22nd July 2021

Head of Communication Department

Erwin Haryono

Executive Director

Information about Bank Indonesia

Tel. 021-131, Email: bicara@bi.go.id