No.

23/241/DKom

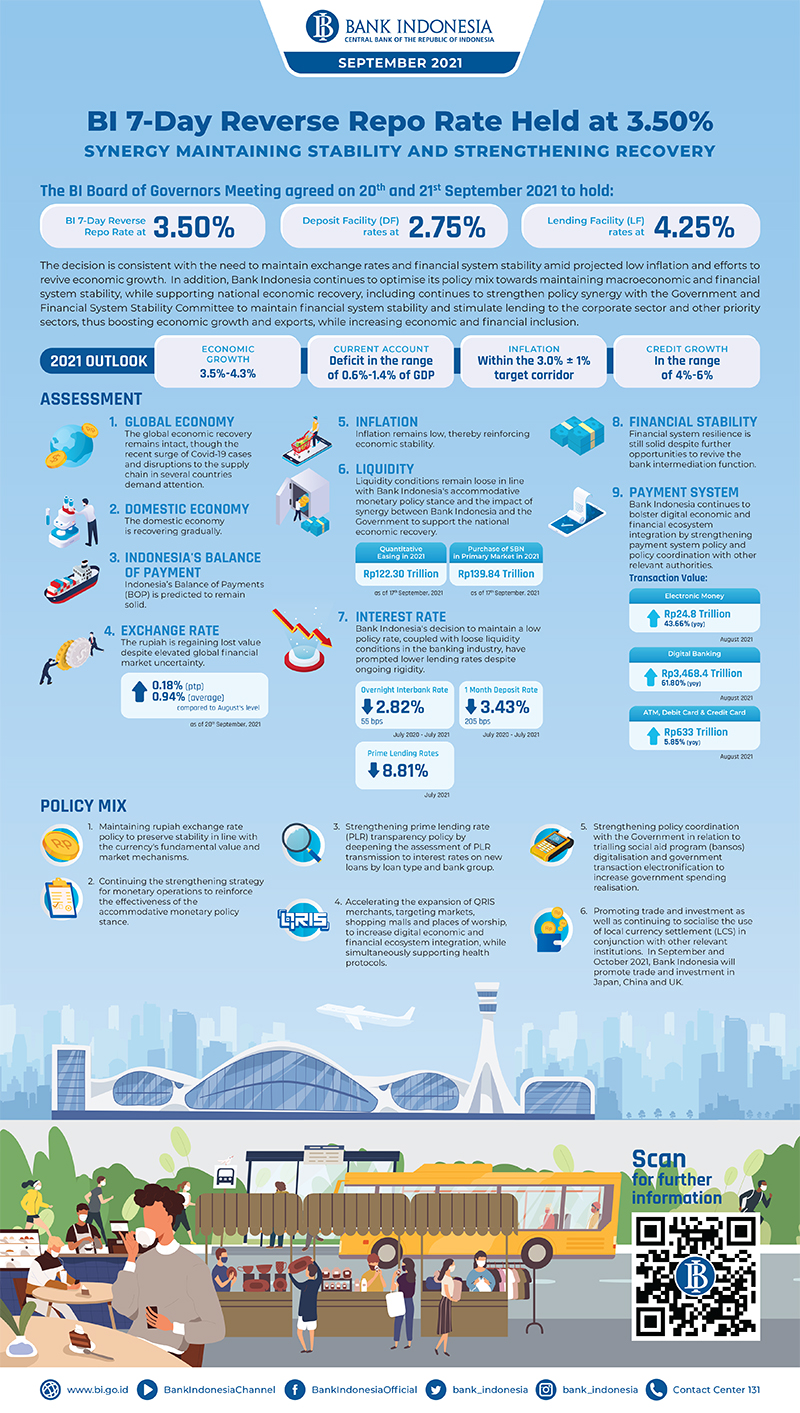

The BI Board of Governors Meeting agreed on 20th and 21st September 2021 to hold the BI 7-Day Reverse Repo Rate at 3.50%, while also maintaining the Deposit Facility (DF) rates at 2.75% and Lending Facility (LF) rates at 4.25%. The decision is consistent with the need to maintain exchange rates and financial system stability amid projected low inflation and efforts to revive economic growth. In addition, Bank Indonesia continues to optimise its policy mix towards maintaining macroeconomic and financial system stability, while supporting national economic recovery efforts through the following measures:

- Maintaining rupiah exchange rate policy to preserve stability in line with the currency's fundamental value and market mechanisms.

- Continuing the strengthening strategy for monetary operations to reinforce the effectiveness of the accommodative monetary policy stance.

- Strengthening prime lending rate (PLR) transparency policy by deepening the assessment of PLR transmission to interest rates on new loans by loan type and bank group (Appendix).

- Accelerating the expansion of QRIS merchants, targeting markets, shopping malls and places of worship, to increase digital economic and financial ecosystem integration, while simultaneously supporting health protocols.

- Strengthening policy coordination with the Government in relation to trialling social aid program (bansos) digitalisation and government transaction electronification to increase government spending realisation.

- Promoting trade and investment as well as continuing to socialise the use of local currency settlement (LCS) in conjunction with other relevant institutions. In September and October 2021, Bank Indonesia will promote trade and investment in Japan, China and UK.

Bank Indonesia continues to strengthen policy synergy with the Government and Financial System Stability Committee to maintain financial system stability and stimulate lending to the corporate sector and other priority sectors, thus boosting economic growth and exports, while increasing economic and financial inclusion.

The global economic recovery remains intact, though the recent surge of Covid-19 cases and disruptions to the supply chain in several countries demand attention. The pace of economic recovery in the latter half of 2021 is slower than previously expected in the US, China and Japan. In contrast, economic recoveries in Europe and Latin America are accelerating, thus underpinning global economic growth. Several early indicators in August 2021, including the Manufacturing Purchasing Managers Index (PMI) and retail sales, remain solid despite the PMI Suppliers' Delivery Times Index pointing to transportation delays. Consequently, Bank Indonesia's global economic growth projection for 2021 remains at 5.8%. World trade volume and international commodity prices have posted strong gains, thus supporting the export outlook in developing economies. Global financial market uncertainty has not fully subsided, impacted by corporate default in China's financial markets, the US Federal Reserve's tapering policy and rising Covid-19 cases. Such conditions are influencing global investor preferences concerning portfolio flows to developing economies.

At home, the domestic economy is recovering gradually. The national economic recovery is influenced by greater public mobility after the Government relaxed virus-related restrictions in response to a flattening of the Covid-19 curve. In August and the beginning of September 2021, domestic economic activity gradually improved after experiencing moderation in July 2021. Such dynamics were captured in several early indicators, including retail sales, consumer expectations, Manufacturing PMI as well as payment transactions through the National Clearing System (SKNBI) and Bank Indonesia – Real Time Gross Settlement (BI-RTGS) system. Concerning the external sector, exports continue to increase on the back of solid demand in Indonesia's main trading partners. Moving forward, the economic recovery is expected to endure given the faster vaccination rollout, persistently strong export performance, reopening of more priority sectors and ongoing policy stimuli. Therefore, the national economic outlook for 2021 remains in line with Bank Indonesia's own projection of 3.5-4.3%.

Indonesia's Balance of Payments (BOP) is predicted to remain solid. The current account is expected to improve, supported by a persistent goods trade surplus. Indonesia recorded its highest trade surplus since December 2006 at USD4.7 billion in August 2021, primarily boosted by a surge of major export commodities, such as crude palm oil (CPO), coal, iron and steel as well as metal ore, despite higher imports stoked by the domestic economic recovery. Meanwhile, foreign capital inflows as portfolio investment have been maintained, recording a net inflow of USD1.5 billion in the period from July to 17th September 2021. The position of reserve assets at the end of August 2021 increased to USD144.8 billion, equivalent to 9.1 months of imports or 8.7 months of imports and servicing government external debt, which is well above the 3-month international adequacy standard. Looking ahead, Bank Indonesia projects a low and manageable current account deficit in 2021 at approximately 0.6-1.4% of GDP, thus supporting external sector resilience in Indonesia.

The rupiah is regaining lost value despite elevated global financial market uncertainty. As of 20th September 2021, the rupiah appreciated 0.94% on average and by 0.18% (ptp) on the August 2021 level. The stronger rupiah is supported by the positive perception of investors concerning the domestic economic recovery, maintained supply of foreign exchange domestically and stabilisation measures implemented by Bank Indonesia. As of 20th September 2021, therefore, the rupiah depreciated 1.35% (ytd) compared with the level recorded at the end of 2020, which is lower than the depreciation experienced in several other peer countries, including Malaysia, the Philippines and Thailand. Bank Indonesia continues to strengthen rupiah exchange rate stabilisation measures in line with the currency's fundamental value and market mechanisms through effective monetary operations and adequate market liquidity.

Inflation remains low, thereby reinforcing economic stability. In August 2021, the Consumer Price Index (CPI) recorded 0.03% (mtm) inflation, thus bringing inflation for the calendar year to 0.84% (ytd). Annually, CPI inflation increased to 1.59% (yoy) from 1.52% (yoy) the month earlier. Core inflation is low and under control in line with compressed domestic demand, maintained exchange rate stability and consistent Bank Indonesia policy to anchor inflation expectations to the target corridor. Inflationary pressures on volatile food and administered prices intensified slightly in response to higher cooking oil prices in line with the international CPO price amid adequate goods supply, as well as the ongoing transmission of higher tobacco duties. Bank Indonesia is firmly committed to maintaining price stability and strengthening policy coordination with the central and regional governments through national and regional inflation control teams (TPI and TPID) to maintain headline inflation within the 3.0%±1% target in 2021 and 2022.

Liquidity conditions remain loose in line with Bank Indonesia's accommodative monetary policy stance and the impact of synergy between Bank Indonesia and the Government to support the national economic recovery. Bank Indonesia has injected liquidity through quantitative easing to the banking industry totalling Rp122.30 trillion in 2021 (as of 17th September 2021). In addition, Bank Indonesia continues to purchase SBN in the primary market to fund the 2021 State Revenue and Expenditure Budget (APBN), totalling Rp139.84 trillion (as of 17th September 2021), with Rp64.38 trillion through primary auction and Rp75.46 trillion through greenshoe options (GSO). The expansive monetary policy stance supports loose liquidity conditions in the banking industry, as reflected in August 2021 by a ratio of liquid assets to deposits of 32.67% and deposit growth of 8.81% (yoy). Liquidity in the economy has also increased, as indicated by narrow (M1) and broad (M2) money supply aggregates, which grew 9.8% (yoy) and 6.9% (yoy) respectively in the reporting period.

Bank Indonesia's decision to maintain a low policy rate, coupled with loose liquidity conditions in the banking industry, have prompted lower lending rates despite ongoing rigidity. In the markets, the overnight interbank rate and 1-month deposit rate have fallen 55bps and 205bps respectively since July 2020 to 2.82% and 3.43% in July 2021. In the credit market, the banking industry continues to lower prime lending rates (PLR) despite rigidity, thus falling from 8.82% in June 2021 to 8.81% in July 2021. On the other hand, banks have begun to reduce interest rates on new loans in line with lower risk perception after the Government started to relax public mobility restrictions. Bank Indonesia expects the banking industry to continue lowering lending rates as part of joint efforts to stimulate lending to the corporate sector.

Financial system resilience is still solid despite further opportunities to revive the bank intermediation function. The Capital Adequacy Ratio (CAR) in the banking industry remained high in July 2021 at 24.57%, accompanied by persistently low NPL ratios of 3.35% (gross) and 1.09% (nett). Buoyed by growing corporate demand for loans in response to greater public mobility, lower interest rates on new loans and lower lending standards, the bank intermediation function expanded 1.16% (yoy) in August 2021, driven by consumer loans and working capital loans that grew 2.84% (yoy) and 1.27% (yoy) respectively. Such developments are indicative of increasing consumption, demand for residential property in particular, along with corporate sector recovery. In addition, MSME loans grew 2.70% in August 2021. Therefore, Bank Indonesia projects credit growth in 2021 in the 4-6% range.

Bank Indonesia continues to bolster digital economic and financial ecosystem integration by strengthening payment system policy and policy coordination with other relevant authorities. Growth of digital economic and financial transactions in August 2021 continued to accelerate given greater public acceptance and growing public preference towards online retail as well as the expansion of digital payments and digital banking. Expansive growth was primarily reflected in the value of electronic money and digital banking transactions. The value of e-money transactions climbed 43.66% (yoy) to Rp24.8 trillion and the value of digital banking transactions soared 61.80% (yoy) to Rp3,468.4 trillion. Meanwhile, the value of card-based payment transactions using ATM cards, debit cards and credit cards stood at Rp633 trillion, with growth of 5.85% (yoy). The number of QRIS merchants continues to expand, growing 120.22% (yoy) to reach 10.4 million merchants in the middle of September 2021. On the cash side, currency in circulation in August 2021 reached Rp843.9 trillion, up 10.73% (yoy). Bank Indonesia continues to strengthen its cash services and distribution strategy amid restrictions on public activity to meet public and banking industry demand for currency.

Jakarta, 21st September 2021

Head of Communication Department

Erwin Haryono

Executive Director

Information about Bank Indonesia

Tel. 021-131, Email: bicara@bi.go.id